APR (Annual Percentage Rate) represents the yearly cost of borrowing money, including interest and fees expressed as a percentage. Understanding APR is crucial because it directly determines how much extra you’ll pay on loans, credit cards, and other debts over time. A lower APR saves you money, while a higher APR can trap you in a cycle of growing debt.

Understanding APR: The Basics

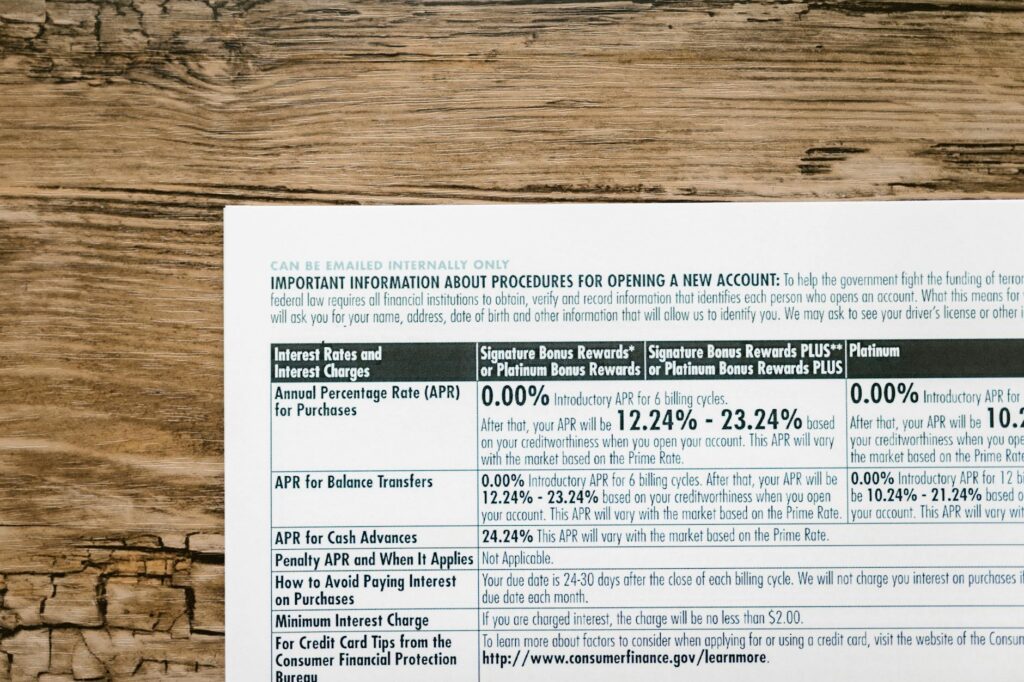

APR is more comprehensive than the interest rate alone. While the interest rate is just the cost to borrow the principal amount, APR includes the interest rate plus other costs or fees involved in procuring the loan. This makes APR the true cost of borrowing.

For example, if you take out a personal loan with a 6% interest rate but there’s a $50 origination fee, your actual APR will be slightly higher than 6%. This difference might seem small, but over the life of a multi-year loan, it adds up significantly.

Credit card companies are required by law to disclose APR clearly, and lenders for mortgages, auto loans, and personal loans must do the same. This transparency helps you compare offers from different lenders fairly. When shopping for debt products, always compare APRs rather than just interest rates.

APR comes in two forms: fixed and variable. A fixed APR stays the same throughout your loan term, making payments predictable. A variable APR can change based on market conditions, which means your monthly payment might increase or decrease.

How APR Directly Impacts Your Debt Payments

The APR dramatically affects how much you’ll ultimately pay for borrowed money. The higher your APR, the more interest accumulates on your debt. Consider these scenarios:

If you carry a $5,000 credit card balance with a 15% APR and only make minimum payments, you could end up paying thousands in interest alone. The same $5,000 at a 9% APR would cost significantly less. Over multiple years, this difference can amount to hundreds or even thousands of dollars.

Your monthly payment amount is also affected by APR. A mortgage with a 3% APR will have a much lower monthly payment than the same mortgage at 7% APR. On a $300,000 mortgage over 30 years, the difference could be $600+ per month—a substantial impact on your monthly budget.

APR also affects how quickly you pay down your principal. When you make a payment on high-APR debt, a larger portion goes toward interest and a smaller portion toward reducing what you actually owe. This is why credit card debt is so dangerous—if you’re only making minimum payments on a card with 20% APR, you’re mostly paying interest while your principal balance barely budges.

This is why paying more than the minimum, or targeting high-APR debts first, accelerates your path to being debt-free. Even small additional payments toward high-APR debt can save thousands in interest.

Strategic Ways to Reduce Your APR and Save Money

You’re not stuck with whatever APR a lender initially offers. There are multiple strategies to lower your rates and reduce debt costs:

Improve Your Credit Score: Lenders offer their best rates to borrowers with excellent credit. If your score is lower, focus on paying bills on time, reducing credit utilization, and checking your credit report for errors. As your score improves, you may qualify for lower APRs.

Shop Around: Different lenders offer different rates for the same product. Take time to compare offers from banks, credit unions, and online lenders. Even a 1% difference in APR can save thousands over the life of a loan.

Balance Transfer: If you have high-interest credit card debt, consider transferring it to a card offering a lower introductory APR. Be aware of balance transfer fees and when the promotional rate expires. This works best if you’re committed to paying down the balance during the low-rate period.

Refinancing: If you have an existing loan with a high APR and your credit has improved, refinancing might lower your rate. This works especially well for mortgages and auto loans where even small rate reductions save substantial amounts.

Negotiate: Don’t hesitate to contact your current lenders and ask for a lower rate, especially if you have a good payment history. Many companies will work with you to retain your business.

Pay Off High-APR Debt First: Use the avalanche method—prioritize paying extra toward your highest-APR debts while making minimum payments on others. This mathematically minimizes total interest paid.

How to Use Our APR Calculator to Plan Your Payoff

Calculating how much you’ll pay in interest on your debts helps you understand the true cost and motivates action. Our debt payoff calculator shows you exactly how APR impacts your timeline and total cost. Enter your current balance, APR, and planned monthly payment to see how long payoff takes and how much interest you’ll pay. You can also experiment with different payment amounts to see how accelerating payments saves interest—this visual proof often motivates people to find extra money in their budgets to tackle debt faster.

Frequently Asked Questions

Is APR the same as interest rate?

No. Interest rate is the percentage cost to borrow the principal amount only. APR includes the interest rate plus other fees and costs involved in obtaining the loan. APR is always equal to or higher than the interest rate. This is why APR is the better number to use when comparing loan offers.

Can I negotiate my APR after I get a loan?

Yes, absolutely. If your credit score has improved, your payment history is perfect, or market rates have dropped significantly, contact your lender and ask for a rate reduction. Credit card companies are particularly willing to negotiate with good customers who threaten to switch cards. Even a 2-3% reduction saves substantial money.

What APR should I aim for?

The “good” APR varies by loan type and current market conditions. Generally, excellent credit scores (750+) qualify for the best available rates. For credit cards, anything under 15% is reasonable if you must carry a balance, though 0% introductory offers exist. For mortgages, rates depend on current economic conditions but anything under 5% is typically competitive. For auto loans, sub-5% APR is good. Always compare your specific offers to current market averages.

- Credit Score Monitoring Service – Credit Karma — Helps users track how APR affects their credit score and monitor interest rates across their accounts in real-time

- Debt Payoff Calculator & Planner — Complements APR education by allowing users to calculate actual debt payoff timelines and compare APR impacts across different payment scenarios

- Personal Finance Management Software – YNAB (You Need A Budget) — Enables users to track debt with different APRs and optimize payment strategies to minimize interest costs based on their understanding of APR

SPONSORED

AI-Powered Credit Monitoring & Repair

Franklin AI monitors your credit 24/7 and automatically disputes errors that may be dragging your score down. Start improving your credit today.

Start Free Trial →Affiliate partner — we may earn a commission at no cost to you.

SPONSORED

Split Purchases Into 4 Interest-Free Payments

Klarna lets you shop now and pay over time — no interest, no fees when you pay on time. Used by 150M+ shoppers worldwide.

Get the Klarna App →Affiliate partner — we may earn a commission at no cost to you.